As mentioned in a previous section, the U.S. went without a proper centralized banking system for nearly an entire century. After the end of the Second Bank, no other notable attempt was made to centralize the banking ecosystem in the U.S. It is for this very reason that the formation of the Federal Reserve marked a huge turning point in the history of the U.S. dollar.

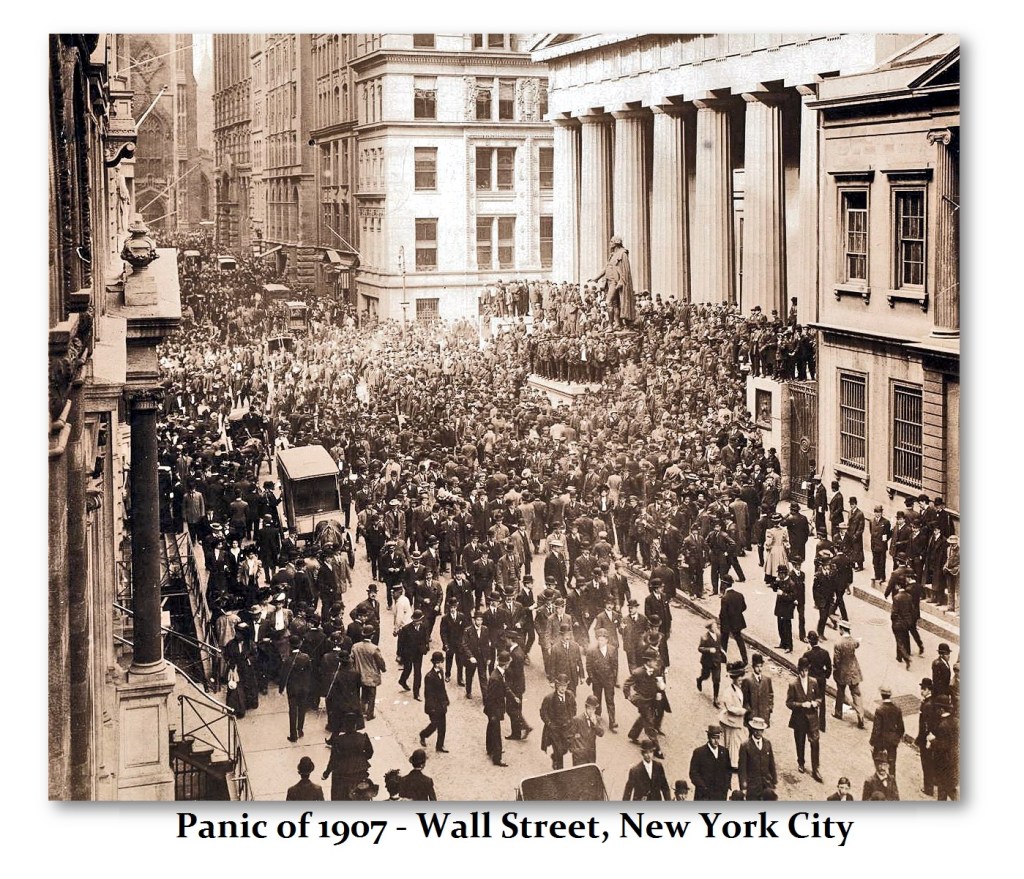

The creation of the Federal Reserve, often referred to as the “Fed,” marked a huge turning point for monetary regulations within the United States. The need arose from the “Panic of 1907,” the first major banking panic of the 20th century, which happened due to the mass failure of banks and trust companies in New York. Trust companies during this time managed more than assets and estates; they also fulfilled many banking roles, such as managing deposits and issuing loans. These private corporations competed directly with banking institutions, which is why the failure of Knickerbockers Trust, the third-largest trust company, caused public confidence in the entire financial sector to plummet. The loss of trust triggered bank runs, an event where large amounts of customers withdraw their deposits from banks, across the U.S., leading to widespread bank and trust failures. However, the situation was prevented from worsening through the intervention of major bankers and investors, most notably J.P. Morgan, who issued millions in loans and deposits to banks and trust companies. This panic, alongside the many crises of the 19th century, pointed out the major vulnerabilities of the current banking system, leading to the Federal Reserve Act of 1913.

Since Andrew Jackson’s termination of the Second Bank of America, no attempt at a central bank had been made for nearly 80 years. The National Banking Act of 1864 allowed the government to supervise and intervene in the banking industry, but it still failed to establish a central financial institution. One of the essential roles of a central bank, alongside regulating money supplies and supervising other banks, is to act as a lender of last resort by providing money to banks in situations of financial distress. This implies it may have been entirely possible to prevent the Panic of 1907 from occurring had the U.S. managed to form a central bank before the 20th century.

Six years after the disaster, Congress passed the Federal Reserve Act, creating the Federal Reserve, an independent institution within the U.S. government. To this day, the “Fed” remains a vital part of the American financial system, serving as the central bank of the United States and working to maintain order in the economy. By creating several Reserve banks in each state and requiring banks to buy capital from those institutions, the Federal Reserve managed to rapidly spread its influence across the country. Furthermore, when it was established, the Federal Reserve also played an essential role in unifying U.S. currencies with the issuance of the Federal Reserve Notes. In a way, these notes were meant to replace the National Bank Notes that were issued by the vast number of federally chartered banks, representing the first step towards creating a single, uniform national currency backed by the central banking system.

Ironically, these notes would become the U.S. dollar used today, rather than the United States Notes. In fact, the term “Federal Reserve Notes” is the proper name for the paper form of the modern dollar. Despite being the first instance of fiat currencies in independent America, the United States Notes did not evolve into the dollar as people know it, but were instead discontinued in 1971. Rather, it was the banknotes originally backed by gold that became the U.S. dollar once the gold standard was abolished internationally in the same year.

References:

Jon R. Moen and Ellis W. Tallman, “The Panic of 1907,” Federal Reserve History, December 4, 2015, accessed October 16, 2025, https://www.federalreservehistory.org/essays/panic-of-1907.

Federal Reserve Act, ch. 6, 38 Stat. 251 (1913)