shattering the golden shell

The gold standard had been a vital anchor to the global monetary system for over a century by the 1920s. Yet, in the aftermath of World War I, with the sole exception of the USA, very few nations had sufficient gold reserves to support their currencies. The following section will discuss how the separation from gold began in the 1930s.

The gold standard had been the cause for many headaches throughout the years. Examples include, but are not limited to, the Panic of 1834, the controversy surrounding the greenbacks, and the battle between gold and silver by the end of the 19th century. The Great Depression was “the straw that broke the camel’s back,” though it was quite a large straw, as in 1933, President Franklin D. Roosevelt signed Executive Order 6102, outlawing private ownership of any gold coins, bullion, or certificates. “Private ownership” applied to any individual or corporation, which meant that the only organization that was allowed to “hoard” gold was the government. Within the Order, President Roosevelt outlined four exceptions, that being:

(1) gold required for industrial or artistic purposes

(2) gold quantities or certificates that did not exceed $100 in value

(3) gold belonging to a recognized foreign government, central bank, or the Bank of International Settlements

(4) gold used for industrial or export purposes, provided the individual obtained proper licensing.

People were required to turn in any gold that did not qualify as any of the exceptions listed above to the nearest Federal Reserve Bank, and in return, they would be compensated with paper money. If they did not, it was possible that they would face up to $10,000 in fines or even jail time. Once the Order was in effect, it removed most gold from circulating in the economy as legal tender, although for the moment, individuals were still able to settle what small debt they had with the gold coins or certificates they still held.

President Roosevelt’s decision marked the “beginning of the end” for the gold standard, as a year later, on January 30th, 1934, Congress passed the Gold Reserve Act. In essence, the Act served to completely sever the link to gold domestically, as it specified that no currency within the U.S. could be redeemed for gold, with exactly one exception of the Federal Reserve’s gold certificates used by the U.S. Treasury for times of need. Additionally, the Act forbade further minting of gold bullion and required the Federal Reserve to surrender its gold to the U.S. Treasury.

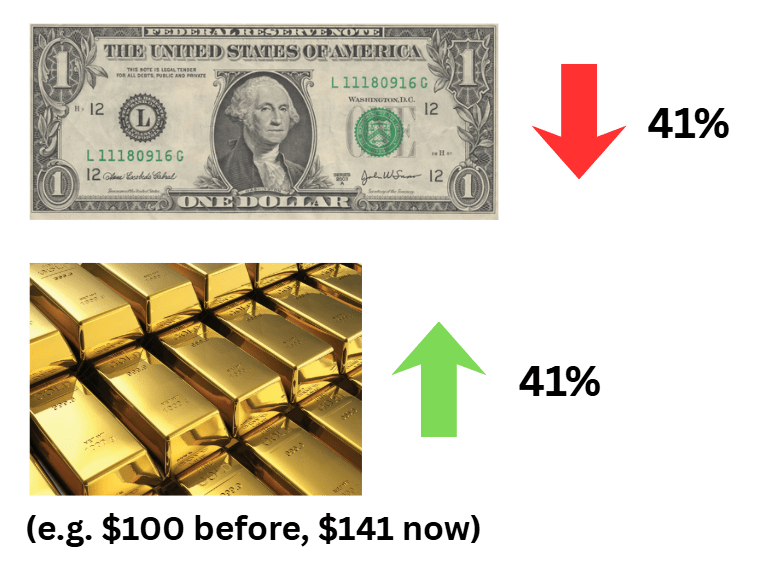

In addition, the Act granted the President the ability to change the ratio between gold and dollar, a power that would immediately be put into effect as President Roosevelt proceeded to devalue the U.S dollar from $20.67 per fine ounce of gold to $35, decreasing its worth by 41%. Despite the negative connotation, the change helped to support the exhausted U.S. economy by allowing every ounce of gold to be worth more in dollars, increasing America’s money supply by that same amount. As a result, the country managed to offset its severe deflation with severe inflation, signaling the start of recovery from the Great Depression. Moreover, U.S. exports became more competitive as they were now much cheaper, supporting farmers and workers across the country. Many foreign governments criticized the change as any asset they held (excluding gold) denominated in U.S. dollars was similarly devalued, but most others saw it as a necessary course of action considering the situation at the time.

Despite the act removing gold convertibility, the Act still required reserves to be held to back U.S. currencies such as the greenbacks or Treasury Notes. Since Americans could no longer redeem their money for gold, the backing was done to reinforce trust within the dollar itself, forming a near-fusion between representative and fiat money. This provides an odd yet accurate parallel to the present day, as, comparatively, currencies today are simply backed by the faith of the people in their governments. We do not question the worth of the money that we carry because it has been ingrained within us that money is valuable. People of the earlier eras placed far less faith in paper money, as evidenced by the myriad of panics and crises triggered by a debased or unstable currency. This is why, despite the dollar’s loss of direct convertibility, gold backing was still required as a guarantee to the people on how the money they carry still held value, working as a symbol of strength and influence of the government.

The U.S. was not alone in its venture, as three years before the Gold Reserve Act, the British abandoned the gold standard completely. The pound at this point was considered overvalued against the dollar, as when the pre-war parity was restored, the British economy was far from what it was before 1914 and could not justify such a high valuation. This hurt exports, increased unemployment, and ultimately made the gold standard unsustainable, leading to its collapse in 1931. Although, unlike America, Britain took a much more drastic step as it completely removed any backing or convertibility to gold, making the pound a complete fiat currency and allowing its value to float freely (with close supervision from the government). Similarly, Japan, Argentina, Australia, and many Scandinavian nations also fully dropped the gold standard during this time.

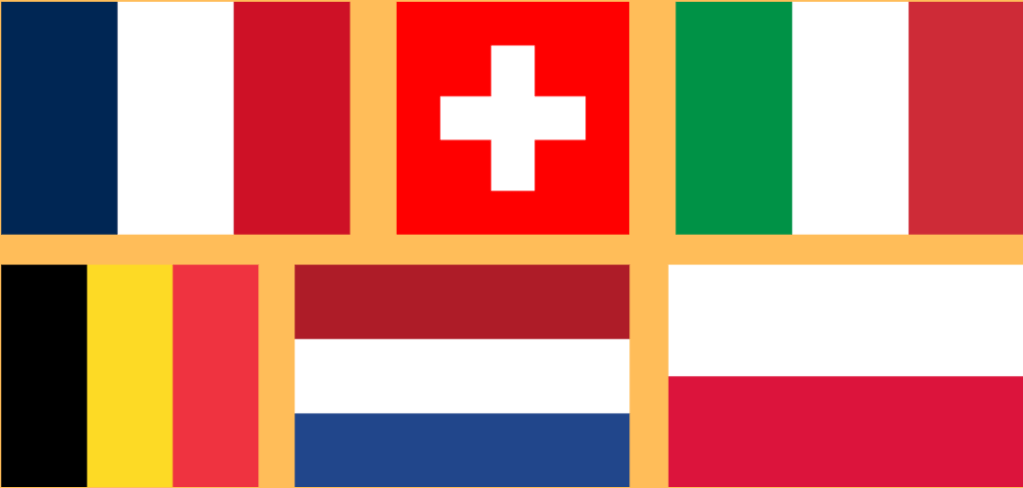

In contrast, France, Switzerland, Belgium, the Netherlands, Italy, and several others formed what is referred to as the “Gold Bloc.” These countries continued to peg their currencies against gold, leading to rigid and overvalued currencies. Table 2 shows that for at least a few years, the Gold Bloc managed to maintain impressive reserves, as by December 1934, the sum of all gold held by just those 5 countries reached an equivalent of $7,810.5 million, nearly equal to that of the U.S., with France alone contributing around $5 444.8 million in gold. However, as investors took their capital to other, more liquid assets in countries like the U.K. and the U.S., gold would proceed to flow out of the Bloc. The resulting deflation, trade imbalance from overvalued money, and wave of unemployment, eventually forced the Bloc to abandon gold altogether.

Abolishing the gold standard meant that FX rates were no longer fixed and there would be nothing to connect one currency to another, creating widespread deflation as governments had little experience in managing floating currencies. As a result, three major Western powers in the U.S., the U.K., and France signed the Tripartite Agreement in 1936, wherein each country pledged to consult one another before making adjustments to monetary policies and avoid competitive devaluations between their currencies. Several other nations, including Belgium, Switzerland, and the Netherlands, would later formally adhere to the treaty, and others would follow the same principles without issuing a formal notice. The agreement itself did not enforce any regulations targeting FX rates, nor did it require any specific action to be taken by each government. One could even argue that the treaty stayed intentionally vague in order to not over-restrict the parties involved, for essentially, these countries had made a promise to talk before acting. Despite its non-binding nature, most governments agreed to cooperate to solve an unprecedented issue, leading to global exchange rates stabilizing over the course of the next 3 years.

As refreshing as it was to see nations unite after the Great Depression, this was not to last. On September 1, 1939, the German invasion of Poland began, marking the beginning of World War II.

References:

Franklin D. Roosevelt, Executive Order 6102—Forbidding the Hoarding of Gold Coin, Gold Bullion and Gold Certificates, April 5, 1933, The American Presidency Project, https://www.presidency.ucsb.edu/documents/executive-order-6102-forbidding-the-hoarding-gold-coin-gold-bullion-and-gold-certificates.

Gold Reserve Act of 1934, Pub. L. No. 73-87, 48 Stat. 337 (1934).

Paul Hallwood, Ronald MacDonald, and Ian Marsh, “Did Impending War in Europe Help Destroy the Gold Bloc in 1936? An Internal Inconsistency Hypothesis,” Working Paper 2007-23, Department of Economics, University of Connecticut, June 2007, https://opencommons.uconn.edu/econ_wpapers/200723.

“Tripartite Financial Stabilization Agreement by the United States, France, and the United Kingdom, Set Forth in Simultaneous Statements, September 25, 1936,” in Foreign Relations of the United States, Diplomatic Papers, 1936, General, British Commonwealth, vol. 1, ed. Department of State (Washington, DC: Government Printing Office, 1953), 258–263.